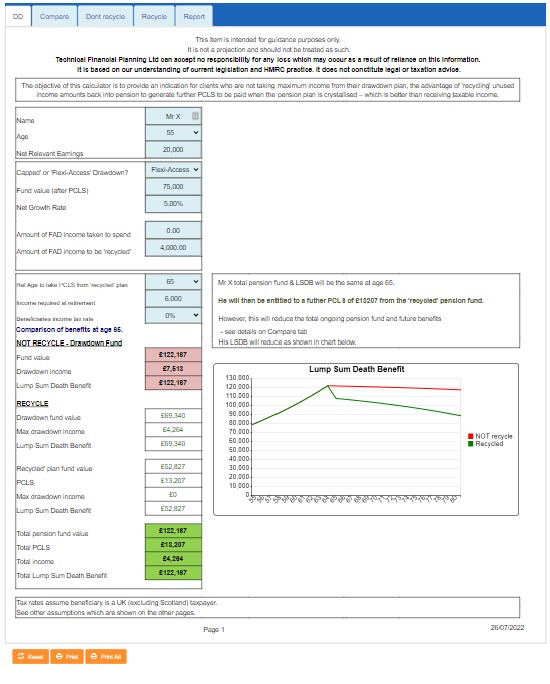

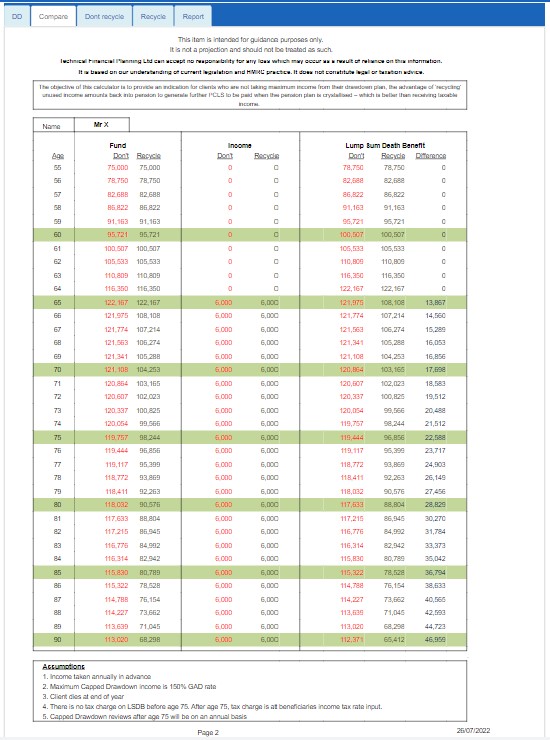

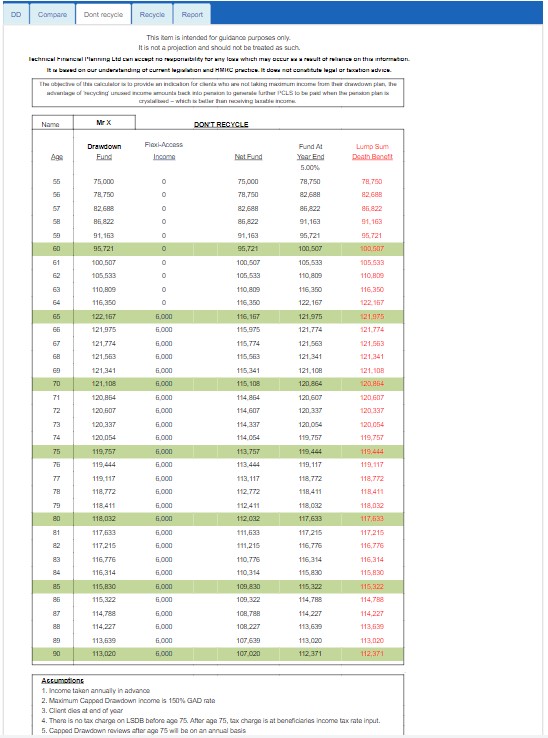

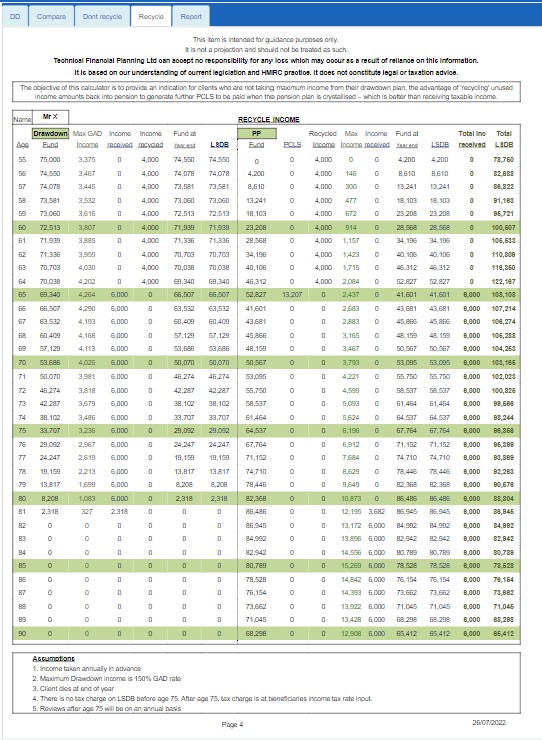

The Recycle Drawdown Income calculator provides an indication for clients who are not taking the maximum income from their drawdown plan, the advantage of ‘recycling’ unused drawdown income amounts back into a pension to generate further Pension Commencement Lump Sum (PCLS) to be paid when the pension plan is crystallised later – which is better than receiving taxable income.

Background

Since April 2006 it is possible for clients to take their PCLS without having to take any drawdown income.

Therefore, for those clients who are not taking their maximum drawdown income, they should consider ‘recycling’ any unused income back into another pension plan.

Since 6/4/2015, death benefits for crystallised & uncrystallised funds are taxed in the same way, so there is now no difference in this respect.

However ‘recycling’ income does still allow a further amount of PCLS when the pension plan is crystallised. Of course, taking this additional PCLS amount would reduce any further benefits payable from the pension plan.

The level of gross contribution that an individual can pay to pension is £3600 or 100% of their salary whichever is the greater

If income is withdrawn from a Flexi-Access Drawdown (FAD), then this will trigger the current Money Purchase Annual Allowance of £10,000.