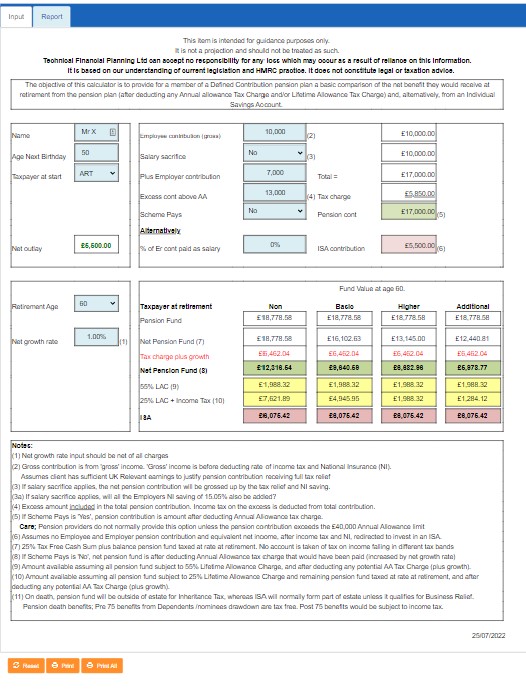

Normally it can be quite straightforward to compare the tax advantages of whether an individual should stay in a Defined Contribution pension plan and continue contributing or to opt-out.

For example. Assuming a gross contribution of £10,000, and at retirement (ignoring tax efficient growth) the benefits will be taken as 25% tax-free cash of £2,500 plus £7,500 subject to income tax. Depending on their tax status at outset and at retirement, the net outlay/ contribution and net benefit would be;

| Basic Rate Taxpayer |

Higher Rate Taxpayer |

Additional Rate Taxpayer |

|

| Net Contribution | £8,000 | £6,000 | £5,500 |

| In retirement; | |||

| Non Taxpayer | £10,000 | £10,000 | £10,000 |

| Basic Rate | £8,500 | £8,500 | £8,500 |

| Higher Rate | £7,000 | £7,000 | £7,000 |

| Additional Rate | £6,625 | £6,625 | £6,625 |

Therefore, normally, a client would be better off staying in the pension plan as the net benefit at retirement would be greater than the net outlay/contribution – unless a BRT is going to be an HRT or ART in retirement.

But what if the pension fund contribution is subject to an Annual Allowance (AA) Tax Charge.

Then this could have an impact on whether the individual would want to continue contributing to a pension scheme.

In some cases, the client may be better off opting out of the pension scheme and investing their net income in, say, an Individual Savings Account (ISA), because the net benefit of the ISA is greater than the net benefit of the pension after taking account of an Annual Allowance Tax Charge.

Of course, if the employer is paying a pension contribution then the employee may be better off staying in the pension scheme – depending on how much of the overall contribution the employer is paying.

Consideration should also take into account whether the employer offers an alternative arrangement e.g. additional salary, rather than an employer pension contribution.

So the situation isn’t straightforward, you have to consider;

- How much of the pension contribution is not subject to a tax charge? (as part will be within the unused AA available)

- How much of the overall pension contribution is paid by the employer?

- Will the employer offer pension contribution on a salary sacrifice basis? (as there’s a benefit in EE NI saving)

- Will the employer contribute his salary sacrifice NI saving?

- Whether the individual is able to use the Scheme Pays facility? As pension providers do not usually provide this option unless the excess is a result of exceeding the £60,000 AA limit.

- Will the employer offer an alternative arrangement to a pension contribution? i.e. pay an additional salary.

The “Continue contributing?” calculator will look at the expected net benefit taking into account the above considerations.

Of course, there are other considerations to be taken into account, for example;

- pension contributions paid by the individual can reduce their ‘adjusted net income,

- Opting out could increase an individual’s estate and their potential Inheritance Tax liability