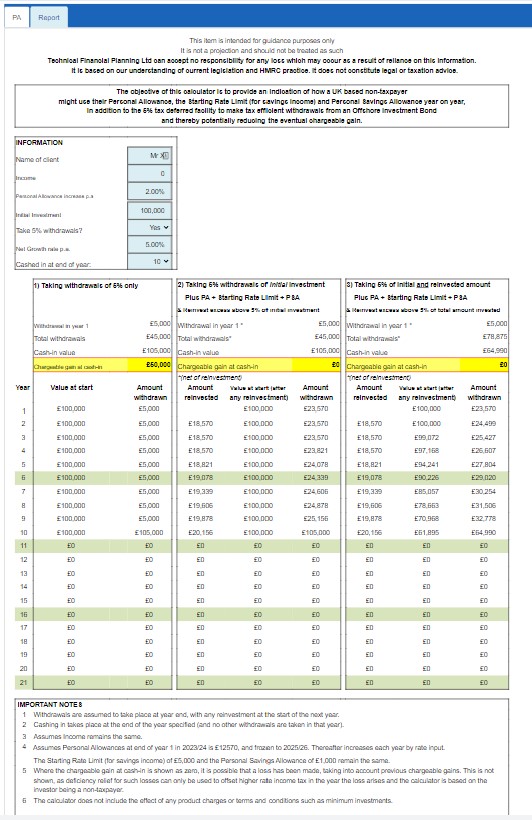

The Offshore Bond utilising Allowances calculator provides an indication of how a UK-based non-taxpayer might use their Allowances to potentially reduce the eventual chargeable gain.

Offshore Investment Bonds can be very useful investments when arranging financial plans for UK-based Non-Tax Payers.

Allowances

This is because Non-taxpayers are able to utilise any of their unused Personal Allowance, Savings Rate Limit (for Savings income) and Personal Savings Allowance against the Chargeable Gain of an Offshore Investment Bond. Of course, if these allowances aren’t used each tax year then they will be lost.

‘Rebasing’

Therefore consideration should be given each tax year for a client to Partially Surrender, in addition to any unused 5% withdrawals, an amount from the Offshore Investment Bond to utilise any of their unused allowances available. The surrender amount can then be reinvested back into the Offshore Investment Bond.

By reinvesting the proceeds as an additional investment, there is no issue of ‘bed & breakfasting’ as there is for Collectives, and the Chargeable Gain (and tax) on final Full Surrender of the Offshore Investment Bond will be lower – see case study.

The Offshore Bond utilising Allowances calculator will provide an indication of the Chargeable Gain the individual will have on final Full Surrender of an Offshore Investment Bond depending if they are;

a. Taking no withdrawals or

b. Taking 5% withdrawals.

However, it will then also show that with planning, the eventual Chargeable Gain on final Full Surrender can be reduced or even eliminated.

This can be achieved by the client taking higher withdrawals so that they utilise their allowances and then reinvesting the excess withdrawals that are not required back into the Offshore Investment Bond.

Also reinvesting the excess withdrawals back into the Offshore Bond will result in a higher ‘initial’ investment which means that, if the client is taking withdrawals, they could receive a higher amount as they could consider taking 5% of the initial investment and 5% of the additional investment amounts.